12th August 2015. This editorial on the ecological economics and social impacts of the global mining industry was published in the July/August edition of the socialist Hindi magazine Samayik Varta. Please click the link to read it in Hindi or download a PDF version of the article here: Prosperity or plunder? The real story behind the global mining industry

Prosperity or plunder?: The real story behind the global mining industry

Samarendra Das and Miriam Rose, Foil Vedanta

Foil Vedanta is a grassroots international solidarity group based in London. We aim to hold the FTSE 250 UK listed company Vedanta to account by building a global movement of communities opposing its operations, and using scholar activism to expose the real interests behind Vedanta and other mining companies. In 2014 our report Copper Colonialism: Vedanta KCM and the copper loot of Zambia, which followed our visit to Zambia, ignited protests and helped change Zambian mining policy.

A history of mining:

Scientists still don’t fully understand how the deposits of precious metal in the Earth’s surface were formed, but the most recent theory suggests that they were brought to the Earth by enormous meteors which smashed into the planet 200 million years after the earth formed (4.3 billion years ago).1 The earth’s crust is mostly made up of Oxygen (47%) and Silicon (28%), followed by Aluminium (8%) and Iron (5%). Other metals are much more rare; Copper makes up 0.01%, Zinc 0.004%, Lead 0.002%, Tin 0.001%, Thorium 0.001%, Uranium 0.0004%, Silver 0.00001% and Gold 0.000001%. Only a fraction of these percentages are to be found in densities which are economically viable to extract.

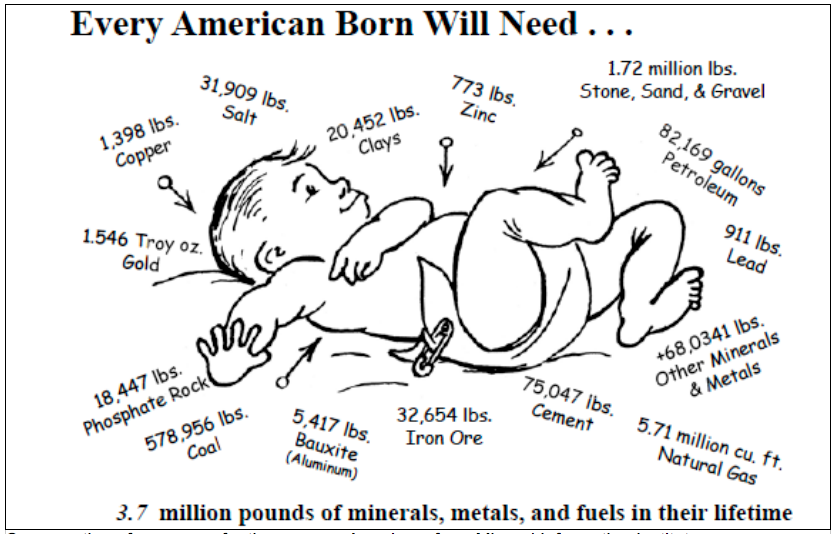

In other words, metals are a very rare and very precious resource on our planet, and are completely irreplaceable. However, in 2014, after only a century of industrial scale mining, the speed and scale of extraction of metals has become so immense that most metals are predicted to run out in the next few decades. For example between 1.1 and 1.3 billion tonnes of aluminium has been extracted historically (until 2014), and at the current extraction rate of 40 – 46 million tonnes per year the remaining 8 billion tonnes will be used up in 20 – 40 years.2

Contemplating the forested and bauxite filled mountain where his community live in Odisha’s Eastern Ghats, Kucheipadar village Deka musician and elder Salu Majhi reflects on this fact saying; “use all this up in 25 years? Very clever my friend.”

However, the modern notion of ‘development’, backed by the World Bank, IMF and UN, suggests that the evolution of the human race is directly linked to their consumption of mined resources. Developmental progress is measured against European or American norms of metal consumption per person per year, aiming for 15 – 35kg of aluminium3, 300kg of steel4 etc. Mining is promoted as an unavoidable and essential part of economic development for countries with mineral resources, highlighting its role in job creation, tax contribution and national self sufficiency. The only issue raised is how to improve the legacy and image of the mining industry, which, it is admitted, is a somewhat dirty business.

From an environmental perspective mining is essentially ‘topocide’, the deliberate administrative destruction of a landscape5. The prevalence of topocide in modern history has defined the current geological period the anthropocene – an era defined by human disturbances to the geological profile and human impacts on nature.

This essay examines some of the key issues with mining, focusing on the three major metals: iron (steel), aluminium and copper. We look at the valuation of mined resources; the link between mining and colonialism, conflict and war; price and market manipulation; the problem with taxation and royalty systems; the mining PR machine; the real interests behind mining companies, and some of the worst mining scandals of recent times.

BOX 1 – Roots of modern mining:

Quarrying and mining go back to Neolithic times. The Azteks are famous for their gold, and later the Romans for their tin and lead. However large scale modern mining did not come into practice until the late 1800s.

The Mesabi mountains around Lake Superior, known to the local Ojibwe people as Misaabe-wajiw, meaning “giant mountain” were the site of America’s first major iron ore mines. These deposits were exploited by the original ‘robber barons’ like Carnegie and Rockefeller (early capitalists accused of enriching themselves at the great cost of the labourers and communities) to provide steel for the Pacific Railway and the civil war effort during America’s ‘Gilded Age’. Later these deposits would be crucial for America in the world wars, along with Pennsylvanian coal.

The link between iron ore and war was made conscious after the First World War when it was declared in 1919 that no country should have a monopoly on iron and coal (which Germany had attempted by annexing the Alsace Lorraine region of France) as it was bound to lead to the stockpiling of munitions and armaments, which was deemed to have partly caused the war.

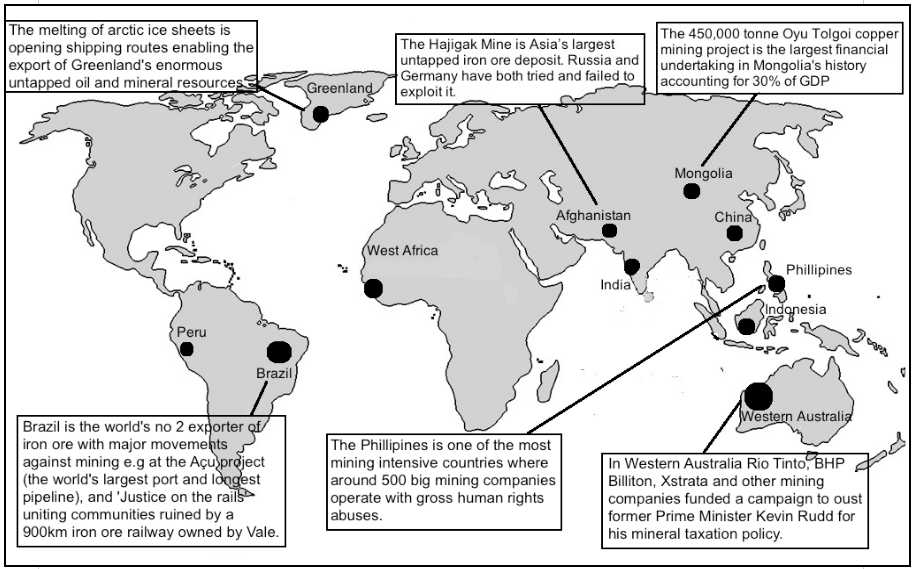

Mesabi’s high grade iron ore ran out in 1952, the same year that Lang Hancock discovered the rich iron deposits of the Pilbara region in Western Australia. Aboriginal populations had occupied these lands for 40 – 50,000 years and the word Pilbara comes from the Nyamal and Banyjima languages meaning ‘dry area’. In the 1960s the Pilbara deposits were considered one of the largest ore bodies in the world of up to 24 billion tonnes. According to the Australian Bureau of Agricultural and Resource Economics in 2010, that resource is being used up at a rate of 324 million tonnes a year, and is expected to be exhausted within 30 to 56 years. Ongoing disputes between Aboriginal groups and the Australian government have raged in the Pilbara, where first nations people like the Yindjibarndi demand some profit share from mining in their sacred lands. Others fear that, like in Mesabi, Pilbara’s migrant labour force will leave ghost towns when the ore runs out. Mineral geologists talk about today’s mining frontiers as the search for ‘new Pilbaras’. The new Pilbaras of today include the mineral riches beneath Greenland’s melting ice, West African iron ore, and even efforts to mine meteorites.

Mining and resource extraction were central to colonialism, and today’s corporations (backed by international institutions like the IMF) are a direct descendent of this tradition, termed ‘neocolonialism’. In Zambia the British South African Company administered Northern Rhodesia and its copper mines with paramilitary forces until 1924, when it was replaced with direct British rule, but continued to own Zambia’s railways until 1947, and their mineral rights until 1964 when Zambia achieved independence. In 1965 Zambia joined the IMF, and when its attempts to form a copper cartel with Zaire, Peru and Chile to increase revenues from mining were undermined, they were forced to privatise all the copper mines through ‘structural adjustment’ policies pushed by the IMF and World Bank. Today copper continues to flood out of the country, bringing enormous profit to foreign owned companies and their shareholders, while Zambia is blighted by poverty, with an average life expectancy of 37.

Chapter 1 – Mining and the market

The theory of ‘resource curse’ has gained immense credibility in recent years. Respected academics such as Paul Collier and Michael Rose have theorised how countries or regions with natural resource wealth often become ‘failed states’ due to corruption, poor governance, inequality, and political violence, and recommend ways to raise revenue and transparency through taxation. Our opinion is that these theses over-emphasise the role of domestic governments and fail to take account of the importance of historical colonial relationships and colonial mentality, issues of ownership and control structures (shareholders etc) and the role of aggressive international policy and finance in creating the unequal dynamic. In this section we will show how metal prices and taxes are manipulated by mining companies and the interests behind them to enable maximum private profit at the expense of local communities and national exchequers – from manufacturing and promoting demand to forming cartels, price fixing mechanisms and monopolies. In addition we will challenge the common focus on tax income from mining, asking deeper questions about who owns the resources, and how they are valued.

Cartels and price fixing:

It is the paradox of capitalism that those who call most fiercely for free-markets are usually the ones most invested in controlling them for their own benefit.

In America a series of aluminium cartels comprised of private companies backed by the US government kept the price of bauxite as low as possible from the 1890s onwards. Most recently in 1994 (by which time protectionism was considered morally wrong and anti-capitalist) the head of Alcoa Paul O’Neill masterminded a US controlled cartel designed to stop Russia from undercutting US prices and flooding the market with surplus military aluminium. The cartel aimed to restrict supply by giving quotas to each country. O’Neill later became the Treasury Secretary under George W Bush.

Up to a quarter of the world’s available aluminium is stored in a network of warehouses owned by the bank Goldman Sachs as part of their ‘futures market’6. ‘Warehousing’ enables control of the price of the metal on the market as supply can be restricted or released at various times. It also enables the banks to make vast profits on speculation and futures markets. Goldman Sachs’ aluminium futures market is estimated to have cost consumers billions of dollars in price hikes, as market manipulations send prices soaring.

Banks JP Morgan and Goldman Sachs, and the world’s largest investment company Blackrock are currently working together in an attempt to buy up 80% of available copper on behalf of investors, and hold it in warehouses. This will create a copper futures market enabling speculation, futures trading, and backing of new loans and funds. In 2010 JP Morgan bought more than half of the available warehoused copper in a few weeks, leading to a spike in copper prices. 7

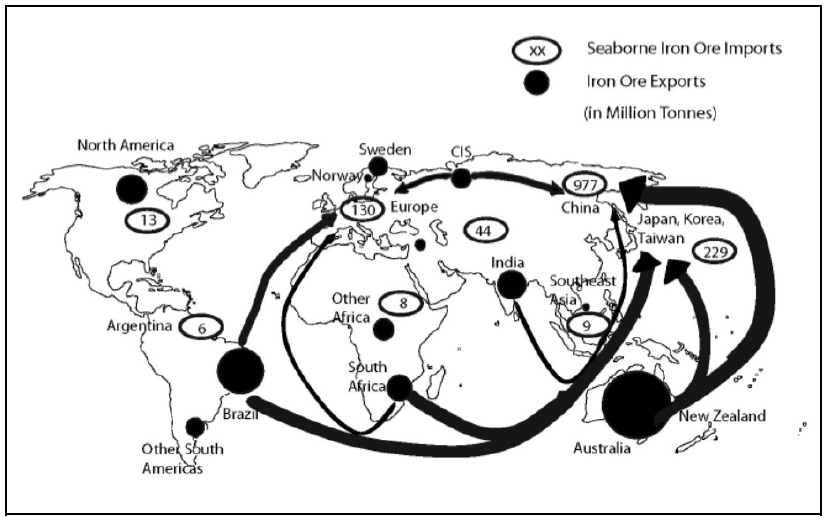

The world’s biggest iron ore miners BHP Billiton and Rio Tinto virtually control the global price of iron ore. The current low price of iron ore is speculated to have been partly created by BHP and Rio by ramping up their iron ore production, flooding the global market and depressing prices. Low prices will put competitors out of business or force them to sell mines, while BHP and Rio weather the self-created storm due to their low production costs.8 Arcelor Mittal and Tata have recently started hedging and trading in iron or derivatives, a market which is expected to reach 1 billion tonnes (of derivatives) by next year, compared to 1.3 billion tonnes of real ‘seaborne’ iron ore traded each year. Derivatives are a complex trading mechanism involving risk insurance, futures trading and other market distortions.9

Aggressive corporate practices such as these have inevitably led to natural resources being concentrated in fewer and fewer hands, which are increasingly able to control global supply, pricing and mining policy. Rio Tinto bought Canadian aluminium company Alcan for $38 billion in 2008, BHP Ltd. merged with Billiton PLC in a $11 billion transaction in 2001 to form the world’s largest mining company; Vale bought Inco Ltd. for $18 billion in 2006 and Freeport-McMoRan Copper & Gold Inc. bought Phelps Dodge for $23 billion in 2007.10 The big three iron ore miners Rio Tinto, BHP Billiton and Vale control nearly 70% of seaborne iron ore trade.

Boom and bust:

The extreme volatility of market-based global metal prices, then, has winners and losers. Aluminium prices for example reached $3,291 per tonne in July 2008 falling down to $1,300 per tonne in 2009. The price crash led to $25 billion losses for Rio Tinto, following their poorly timed purchase of rival company Alcan (who made $38.1 billion out of the deal), and left smelters in Iceland rusting half built, and bauxite mining countries being told their ore was worthless. In 2014 the top mined resources have lost $200 billion in value due to China’s economic slowdown.11

In the case of iron ore the China boom created partly by the construction spree in the years leading up to the 2008 Olympics led to a ‘gold rush’ on iron ore in India, which was selling 91% of its exported iron to China at the time. The now well documented result was a feeding frenzy of private mining companies seeking to exploit the high profit margins with little or no regard for the law or the social and environmental impacts. The Shah Commission inquires into

iron ore and manganese mining in Odisha and Goa, and the Lokayukta report in Karnataka revealed the massive scale of illegal mining taking place and the blatant disregard for Environment Protection and Forest Conservation Acts by local officers, as well as state governments and even the Ministry of Environment and Forests. The state and national exchequers lost out on taxes to the tune of millions of dollars and the iron ore reserves were massively depleted.

In Goa 18% of the tiny state, largely made up of the Western Ghat mountains had been damaged by mining activities with 182 licenses to extract 66 million tonnes per year issued, and much more being mined in reality. $5 billion of taxes was lost to the exchequer. And at the rate of extraction in 2011 the iron ore would have been used up in 9 years. Five or six families were reported to be profiting from 90 mining leases, and many other leases were handed from private individuals to big mining companies with major kickbacks. Vedanta’s Sesa Goa was exporting nearly 50% of Goa’s iron ore. Meanwhile 1600 cases were filed against anti-mining villagers in one village alone.12

In Karnataka the Bellary region became ‘a republic of lawlessness’ with clearances for 82 million tonnes of iron ore per year issued and controlled largely by mining barons and State government ministers the Reddy brothers.13 Thousands lost their farmland and homes to mines and nothing could be grown in the dusty and polluted fields. When mining was eventually banned thousands of miners returned to their former livelihoods in farming. Interestingly revenue for the State even increased after the ban, showing the degree of looting taking place.14

In Odisha the mining scam is estimated to have been worth $48 billion and Chief Minister Naveen Patnaik has issued an invoice for $9.6 billion in lost taxes.15

Tax injustice:

Debate on the economic benefits of natural resource wealth almost never strays far from the concepts of royalty and taxation. NGOs and major international campaigns such as Tax Justice Network and the Extractive Industries Transparency Initiative (EITI) have played into this ‘rent seeking’ ideology, lobbying for minor increases in tax revenues, and ignoring more profound issues around the ownership and valuation of mineral resources at the outset.

In India mining companies are obliged to pay 10% royalty on the selling price of a tonne of iron ore. In fact royalty itself is a colonial concept, which originally meant ‘a percentage of profit gained from a service rendered to the state’. The relevance of royalty was challenged by Indian courts in 1993-4 during a dispute over low royalty and other rental rates for granite mining.16

In Zambia, the world’s eighth largest copper producing country, mining companies like Vedanta’s subsidiary Konkola Copper Mines (KCM) pay royalty rates of only 0.6%, negotiated by the IMF and Clifford Chance in secret ‘development agreements’ fixed for 20 years (until 2018 in KCM’s case). The Zambian government’s current attempt to raise rates to 6% is being vehemently opposed by the IMF and mining companies. Worse, many copper miners don’t even publish their profits and pay virtually no income tax. Vedanta’s KCM have claimed they are making a loss in Zambia (despite global copper prices of over $7000/tonne) and have attempted to fire 2000 workers to save costs. However, in January this year Vedanta boss Anil Agarwal was filmed telling businessmen in Bangalore how he made between $500 million and $1 billion a year from KCM. The video, released by Foil Vedanta sparked major protests and an investigation into the company which revealed some of the ways Vedanta were evading tax by selling copper at a loss to their own subsidiary – Fujairah Gold, controlled by Anil Agarwal’s son Agnivesh in Dubai – who would then sell it on at a huge profit. This is called transfer pricing. Another allegedly common corporate practice in Zambia is failing to declare cobalt and silver which are mined with copper, and then exported as unprocessed ore or waste with no tax or royalty. Vedanta’s accounts (released during the investigation) showed a $6.3 million loss in 2013 and KCM had even refused to pay the state-run energy company Copperbelt Energy Corporation the $60 million they owed.

Income tax and royalty are revenue based taxation systems which are wide open to abuse by financial mechanisms, some of which aren’t even illegal, such as transfer pricing and use of tax havens, mis-declaring of mined and exported ores. The industrial scale loot that results is partly possible because of the paucity of information held by the government. We have argued that Zambia (like India) will never get a fair deal as long as they fail to independently monitor volumes of mined and exported ore, and charge a proper price for the resource.

The EITI, founded by British Prime Minister Tony Blair and the World Bank in 2002, and promoted by thousands of NGOs, aims to increase transparency by asking signatory companies to publish their tax and royalty contributions, and signatory states to disclose what they receive, revealing any discrepancies. Rather than looking at the grossly unfair terms on which mining companies operate, or the network of tax havens (mostly supported by the UK) which facilitate some of the estimated $148 billion per year in capital flight (lost revenue) flooding out of Africa, EITI points the finger at domestic corruption and accuses African politicians of lining their pockets.

Mining finance:

Many mining companies play on their nationality to win preferential treatment by the state. Vedanta, ArcelorMittal and Essar for example are all British companies listed in London but they still use their ‘Indian-ness’ to gain reputation and advantage in India (and Africa) when possible. Conversely they use their British identity to attract finance and gain credibility in international markets. In fact most of the top mining companies are controlled by a very similar and closely linked group of shareholders which are beyond national borders including banks, investment firms, and foreign government pension funds.

An even smaller group of ‘economic hitmen’ whose names are rarely heard have been responsible for many of the biggest mining deals and negotiations. For example Larry Fink, a Washington insider who was named as a potential US treasury secretary, who set up and heads Blackrock, the world’s biggest asset management company, in charge of $4.1 trillion of assets (making it bigger than any bank, insurance company or government fund) and is the majority shareholder in half of the world’s 30 largest companies (including every one of the top mining companies).17 Ian Hannam is responsible for some of the biggest mining deals including the formation of BHP and merger with Billiiton, and launching Vedanta and Xstrata on the London Stock Exchange. He is now pushing mining in Afghanistan. Hannam had to resign his role as chairman of capital markets at JP Morgan Cazenove in April 2012 following evidence for market abuse related to passing on insider information.

Other figures like the investment tycoon and ‘philanthropist’ George Soros play a dangerously conflicted game of both investing in mining, and funding powerful NGO projects (through his Open Society Foundations) who claim to hold mining companies to account. Soros is a private figure who wields enormous financial and political power to influence and even define the discourse on liberalism and mining capitalism.

Chapter 2: Mining and material flow

The speed of extraction:

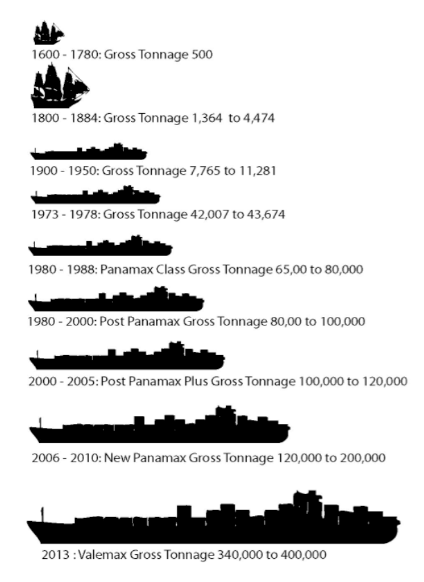

The world’s largest company BHP Billiton celebrated the shipping of its 1 billionth tonne of iron ore to China in December 2014. Chief Executive Andrew MacKenzie was quoted saying that though it had taken 30 years to ship the first 1 million tonnes to China, the billion mark was reached only 12 years later, and the next 1 billion tonnes would be exported within only 5 years.18 As the picture shows, the advance in technology for extracting and exporting ores has enabled extraction rates that could exhaust the world’s supply of metals in a few decades. Vale’s super ships Valemax can export 400,000 tonnes of ore in one load.

The strategic goal of India’s 2005 steel policy was ‘that India should have a modern and efficient steel industry of world standards…with indigenous production of over 100 million tonnes (mT) per annum by 2019-20′. In fact India reached 218 million tonnes in 2009-10, and the proposed new steel policy 2012 aims to achieve a projected production level of 275 million tonnes by 2025?26.19

However, the Shah Commission took expert advice from the Indian Bureau of Mines that at these rates high grade iron ore was likely to run out in only 10 years time, and all iron ore within 57 years (in 2010). The policy was also deemed contrary to the Article 39 of the Indian Constitution which states that “the ownership and control of the material resources of the community [should be] so distributed as best to subserve the common good; that the operation of the economic system does not result in the concentration of wealth and means of production to the common detriment.”

The constitution also states that resource wealth should be conserved and used gradually so as not to disadvantage future generations. The 2008 mineral policy goes further by attempting to redefine this aspect of the constitution, stating, “Conservation of minerals shall be construed not in the restrictive sense of abstinence from consumption or preservation for use in the distant future but as a positive concept leading to augmentation of reserve base through improvement in mining methods, beneficiation and utilisation of low grade ore and rejects and recovery of associated minerals.”20

The obvious question is who has been writing India’s steel policies? Or in whose interest have they been written when their sole purpose seems to be to enable as much extraction as possible. Four drafts of the 2012 national steel policy were submitted to the industry for their editing and agreement21. 2005 steel policy goes on to note that India’s steel consumption was only 30kg per person per year, compared to 150kg world average and 350kg in the ‘developed’ world, and laments that rural steel consumption is only 2kg per person. It suggests a variety of ‘promotional efforts’ to raise steel use to a target of 4kg per year by 2019-20. These statements serve to demystify the notion of supply and demand often used by companies to justify expansion based on the needs of the people. In fact ‘demand’ is manipulated and manufactured by companies working closely with governments for their own interests.

As India’s domestic reserves, and the ‘internal colonies’ created to exploit them, are used up, or policies become less favourable to industry, Indian companies are turning to new frontiers, (neo)colonising parts of Africa, Greenland and Latin America. For example Jindal Group have landed a mega iron ore deal in Afghanistan which has been accused of corruption since the consortium, appointed with public money, is made up of four companies all headed by Naveen Jindal and his relatives.22 Mittal are accused of corruption in Liberia, where they did a $900 million deal for iron ore mines before the civil war had ended23, and are now planning a mega open cast mine in the fragile ecosystem Greenland for $23 billion worth of iron ore.24

Real valuation:

The real cost of mining to national economies and affected communities goes far beyond loss of profit from taxation or export value. The true price of metals includes the pollution of water and air caused by mining and transportation, the cost of decommissioning mines and smelters, health effects on local populations, and the depletion of the finite resource, which will not be available to future generations. These are known as ‘externalities’ – real costs which will be borne by people and governments at present and in the future, but which are not included in the market price of a resource. Ecological economist Maarten De Wit values the real cost of copper (including externalities) at $33,000 per tonne, five times the current market price of $6500 per tonne. The price is high because copper is one of the most material intense metals to produce – creating 500 tonnes of waste, and using 260 tonnes of water, as well destroying 2 tonnes of pure air for each tonne of primary copper. Table 2 shows the impact of all major metals on the ecosystem (material intensity) and the number of years left until they are exhausted at present extraction rates (reserve life index). Understanding the real ecological price of metals is important for resource rich states, since when their resource is depleted, they will continue to pay for the externalities for years to come.

Ecological and heterodox economists have quantified the cradle to grave impacts of metal mining, processing and waste, as well as making alternative evaluations of per capita availability to enable intergenerational equity (ie leave enough for future generations).

TABLE 2: Material intensity and reserve life index of major metals (According to Wuppertal Institute for Climate, Environment and Energy, and JP Morgan reserve life index)25.

| Metal (primary) | Abiotic material (tonne/tonne) | Water (tonne/tonne) | Air (tonne/tonne) | Reserve life index (years) |

| Steel | 6.97 | 44.6 | 1.3 | 80 – 90 |

| Aluminium | 85.38 | 1378.6 | 9.78 | 20 – 40 |

| Copper | 500 | 260 | 2 | 125 |

Real transparency:

One of the most opaque aspects of global material flows is the transportation, sale and export destination of metal ores, often sold in secrecy and at an unspecified price ‘at sea’. Zambia’s Central Statistical Office report that the vast majority of exported copper is destined for Switzerland with only a fraction ending up in China, the world’s largest consumer of copper. In fact Switzerland had no records of the arrival for the vast quantities of metal (which in reality were destined elsewhere), yet it was being sold on by Swiss agencies to other buyers at a grossly inflated rate. If these prices had been realised in Zambia revenue from mining could have been increased six times over. Vedanta sells its Zambian copper ‘off gate’ to a trader or dealer, and claims it has no idea where the metal ends up.

The fact is that most metal is traded on the high seas – a colonial tradition which is almost

totally de-regulated, and unaccountable. For example the contribution of shipping to pollution

and climate change has only recently been established when it was revealed that sixteen mega ships alone produce the same amount of sulphur as all the world’s cars. Global shipping is overseen by the International Maritime Organisation (IMO), a key United Nations body based in London, which has refused to take part in carbon reduction and other regulatory programmes.

The opaque nature of export by sea, and the scale of the iron ore loot of India, is highlighted by two ships which sank in 2009 after loading up with iron ore and were not claimed by any owner. Hong Kong registered ship MV Asian Forest sank off Mangalore with a full load of iron ore fines in July 2009, while MV Black Rose, a Mongolian bulker, sank off Paradip Port in Odisha on 9th September of that year, and was later discovered to have no license or insurance.26 Who owned these ships and where were they headed with their valuable cargo?

In Goa the scale of the mining scam was first revealed when communities started counting the number of trucks and barges leaving the mines and ports, and calculated that the volumes were far above legal limits. Vedanta’s subsidiary Sesa Goa for example are accused of exporting 1.5 crore (15 million) tonnes of iron ore from Goa in 2010/11 while only declaring 76 lakh (7.6 million), their agreed export allowance27.

National governments and citizens of resource rich countries have a right to know how much of their precious resource is being extracted, where it is being sold to, and at what price. They must independently audit mines and ports to establish these essential facts. It is only in the interests of mining companies and their profits to keep this information secret.

Chapter 3 – Managing Reputation

Image is everything: the mining PR machine

Mining is essentially a dirty business. As the last chapter demonstrated, the ecological impacts of metal production (material intensity) are enormous – using and polluting vast amounts of water, air and soil. Producing one tonne of aluminium, for example, produces 82.5 tons of overburden and toxic waste, uses 13,000 litres of water, and produces 20.6 tons of CO2 equivalent28. In addition there tend to be major social impacts – displacement (often affecting indigenous people who live in forested and remote areas where minerals are found), health impacts on surrounding communities, loss of traditional livelihoods (farming, fishing etc) and workers rights issues for mine and metals workers (deaths, low pay, anti-union activities). For these reasons the concept of ‘sustainable mining’ can be seen as a corporate oxymoron.

As the mining industry has shifted from its role in overt colonialism and unequal enrichment, to a new conception as an important part of global development, it has necessarily had to change its image. Today mining and metals lobbies are some of the most powerful global actors, working alongside the World Bank, IMF, and state governments. They use PR agencies, academic institutions and NGOs to gain credibility as a contributor to community development, job creation, and even sustainability, as well as a provider of resources essential to modern life.

The International Council on Mining and Metals (ICMM) is the key lobbying organisation for the industry, particularly on matters of sustainability and the environment. It is based in London and represents most of the major companies and 30 national and regional mining associations and global commodity associations.

ICMM was formed in 2001 following the perceived threat of the World Summit on Sustainable Development (WSSD) in 2002 to the reputation of the industry. This threat led to the formation of the Global Mining Initiative (GMI) in 1999, and spawned industry-friendly research projects funded by mining companies such as the $10 million Mining, Minerals and Sustainable Development (MMSD) project with the International Institute for Environment and Development (IIED), which highlighted the importance of the mining industry to job creation and the global economy and suggested ways to increase transparency, enhance perceptions of sustainability, and gain community support. In 2001 the International Council on Metals and the Environment (ICME) broadened its agenda to incorporate sustainability and reputation concerns and became the ICMM.

One of the contentious areas for the mining industry is the need to gain a social license to operate, under the internationally recognised principle of Free Prior and Informed Consent (part of the Equator Principles for business). Vedanta’s Niyamgiri debacle demonstrated the myriad of ways in which mining companies can seek to manipulate or subvert this process to get their way, but importantly in this precedent case, did not manage to override the will of the community. Critics have noted that without the right to veto a project, which is not included in the Equator Principles, local consultation processes cannot be considered true agreement.29

The huge amount of money spent on mining PR pays off. In Australia a $22 million advertising campaign by the mining industry was successful in stopping the proposed Resource Super Profits Tax, which would have increased tax revenue by $200 billion over the next decade, in light of predicted mining profits of $600 billion in the same period. The expensive PR campaign saved the mining companies $160 billion.30

Corporate Social Relations:

The concept of Corporate Social Responsibility (CSR) became particularly prevalent after the World Business Council on Sustainable Development in 1995 (following the Rio Summit in 1992), which noted that industry had a bad reputation which was affecting their ability to do business. Today ‘reputational risk’ is a key factor in corporate success, as opposition by local communities, or negative global publicity can directly affect share prices. Looking at the websites and PR campaigns of most mining companies you could be mistaken for thinking they are charities, as a fanfare of women’s self help groups, happy children and environmental conservation cover the pages.

CSR is problematic in a number of ways: In many cases the charitable promises are empty, or are abandoned once mining deals have been done or foreign funders impressed (for example corporate built schools and hospitals which lie empty or without staff). In some communities promises of money for self help groups etc are used as a way to silence local opposition to mining activities. Worse still, companies partnering with NGOs can even use ‘stakeholder meetings’ to glean information from local communities, which is later used against them. For example in April 2008 Arcelor Mittal Foundation (Mittal’s CSR wing) organised a stakeholder meeting in Ranchi, Jharkand called ‘Development Initiative for a Better Tomorrow’. 70 local NGOs were invited to the seminar, with the notable exception of the ‘Adivasi Astitwa Raksha Manch’ (Tribal Identity Protection Forum) and heads of tribal councils. Local adivasi activist Gladson Dungdung claims: “The purpose of the seminar was, really, to kill two birds with one stone. It took the local NGOs into confidence and had a peek into the strategies used in people’s resistance, so as to develop its own strategy to counter it.”31

Tripartite partnerships of business, NGOs and government to ‘promote development’ were encouraged by a 2005 UN General Assembly resolution ‘Towards Global Partnerships’. However, while embracing the potential of CSR to enhance profit, industry has also resisted efforts to increase community benefit from CSR. In 2009 the Confederation of Indian Industries vehemently opposed attempts in the Companies Bill 2009 to introduce mandatory spending of 2% of net profits on CSR.32

The complicity of local, national and global NGOs and academic institutions who are funded by the mining industry and/or the institutions or national aid agencies that support the industry, has been called an NGO Industrial Academic complex. The close links can be demonstrated by common board members such as Michael Lynch Bell, a director of disgraced mining company Kazakmhys33 (implicated in the fraudulent activity which resulted in the de-listing of Eurasian Natural Resources Corporation [ENRC] from the London Stock Exchange last year)34 and an Action Aid board member.35

Action Aid have also been criticised for their conflicts of interest in the Niyamgiri campaign. In 2003 they accepted a £40,000 (41 lakh Rs) donation from Vedanta subsidiary Sterlite for homeless shelters in Delhi, while in 2010 Action Aid’s CSR arm ‘Partners in Change’ was part of a jury which awarded Vedanta a ‘Best Community Development’ award for its ‘good work’ around the same Lanjigarh refinery which they were supposed to oppose36, prompting a protest outside Action Aid’s Odisha office that lasted several days.

The Mining industry and their lobbies fund University departments, projects and courses which develop mining technology as well as improving the social reputation of the industry. The World’s fourth largest mining company Vale, for example, has created the Vale Columbia Centre on Sustainable International Investment at Columbia University which also partners with NGOs on the issue. Other major mining funded academic centres include Colorado School of Mines, School of Earth and Ocean Sciences – University of Victoria, University of Eastern Finland, University of Dundee, University of Queensland, University of Vermont – Rubenstein School for the Environment, 37 and Harvard University’s Kennedy School of Government with support from Rio Tinto Corporation.38

The true face of mining: major mining scandals, scams and disasters

Despite the billions spent on mining PR, the industry continues to be rife with stories of corruption, social unrest, poverty and environmental disasters. The continually unfolding tragedy of West Papua’s Ok Tedi mines, and the current iron ore rush on West Africa are two such examples, where Indian (and British-Indian) companies are now also implicated in the fray.

West Papua and Papua New Guinea have been devastated by the human rights abuses and environmental destruction caused by mining companies. In the early nineties Rio Tinto and partner Freeport McMoran caused ‘massive environmental devastation’ at the Grasberg mine in West Papua, and when people rioted over conditions in 1996, began funding the Indonesian military to protect the mine. $55 million was donated by Freeport McMoran to the Indonesian military and police between 1998 and 2004, resulting in many murders and accusations of torture.

Throughout the 1980’s and 1990’s BHP (later BHP Billiton) poisoned and polluted 50,000 people by discharging of over 2 billion tonnes of untreated waste including cyanide into the Fly and Ok Tedi rivers in what was named ‘the world’s biggest environmental disaster’. The Ok Tedi copper and gold mine was one of the world’s largest copper deposits, on Mount Fublian, a sacred mountain for the Yonggom indigenous people in West Papua. In 1996 BHP were sued for $28 million and admitted that 90 million tonnes of waste a year had been released into the rivers, but were granted immunity from further lawsuits. In 2002 BHP Billiton gave their 52% stake in the mine (which they had gradually diluted due to bad publicity) to the Papua New Guinea Sustainable Development Program Limited who continued to run the mine, and dump raw waste into the rivers. In 2007 landowner groups from the Ningerum indigenous people filed suits against BHP Billiton and the operators of the Ok Tedi copper mine for civil damages exceeding US$4 billion, and in 2013 BHP’s legal immunity was removed. Indian consultancy company Wipro Ltd are now partnered with Ok Tedi Mining Limited to develop their plan to extend the mine’s life til 2025.

In 2011 a US federal court action accused Rio Tinto of involvement in genocide in Bouganville, Papua New Guinea, where the government allegedly acted under instruction from Rio Tinto in the late eighties and nineties when it killed thousands of local people trying to stop their Panguna copper and gold mine. 10,000 people were eventually killed in the class uprising that resulted from the conflict over the mine. Rio Tinto were accused of providing vehicles and helicopters to transport troops, using chemicals to defoliate the rainforests and dumping toxic waste as well as keeping workers in ‘slave like conditions’.39

The Simandou mountains in Guinea, West Africa, hold one of the world’s largest tier-one reserves of iron ore at 2.4 billion tonnes. In 1997 the mining lease was awarded to Rio Tinto, but in 2008 was suddenly removed from them by the Guinean government, and awarded instead to Beny Steinmetz Group Resources (BSGR) – a little experienced mining company owned by Israels most wealthy businessman Beny Steinmetz. A year later BSGR had sold a 51% stake in the project, for which he had paid nothing up front, to Vale for $2.5 billion, making an enormous profit. This un-accountable practice is known as ‘flipping’. Evidence later revealed how BSGR had used an aggressive public relations firm called FTI (whose current chairman for the Middle East and Europe – Mark Malloch Brown, is the former Deputy Secretary-General of the United Nations) to bribe President Conde’s wife for the deal. Currently the two Southern blocks of the deposit remain with Rio Tinto, while the Northern blocks are tied up in legal cases between BSGR, Rio Tinto, Vale and the Guinean government.40

Just next door in Liberia, Vedanta have acquired Western Cluster Limited, a company with a 1 billion tonne iron ore deposit, via a similar ‘flip’. Vedanta’s iron mining subsidiary Sesa Goa bought 51% of Western Cluster Ltd from Elenilto Minerals & Mining LLC in 2009 for $90 million, on the same day Elenito signed a 25 year mining lease with the Sirleaf government for the mine. Less than six months later, Elenilto (a phony company set up to facilitate and ‘flip’ the deal) bailed out all together by selling the remainder of the Western Cluster to Vedanta for $33.5 million in cash. Not only is this deal irregular and highly suspicious, but the total $123.5 million Vedanta paid for Western Cluster is a fraction of the real value of the 1 billion tonne reserve.41

A few recent scandals closer to home include Mittal’s so far unsuccessful attempts to displace a large adivasi population for a 12 million tonne steel plant in Jharkhand42, and the dredging of the Baitarani river in Odisha (which serves 5.1 million farmers) by Stemcor (a company part owned by UK MP Margaret Hodge) for a pipeline to carry iron ore sludge to the coast for export.43

The future of mining

As we have noted, popular debate on the costs and benefits of the mining industry rarely stray from a focus on its role in ‘development’ – creating local jobs, contributing domestic tax, and producing mined resources crucial to the growth of ‘developing economies’. At best commentators, including NGOs, recommend an increased tax contribution, and more ethical and ecological mining to improve the image and social value of the mining industry.

In fact there are much more profound questions to be raised about how we value the rare, precious and irreplaceable resources on our planet. We have attempted to show how the extractive capitalist economy relies on externalities (real costs which are not included in product price), and distributes these ecological expenses of pollution, ill health and non-functioning ecosystems disproportionally to indigenous and marginalised populations, and to future generations. We have disputed the concept of ‘supply and demand’ for metals, demonstrating how mining lobby groups work with governments and international institutions to manufacture and promote demand as a definition of human ‘development’. In addition we have noted how many billions of tonnes of metal are already in circulation on the planet, much of which could be recycled and re-used. We have shown how metal prices and the perceived plenty or scarcity of metals are manipulated by banks and investment firms using financial mechanisms such as warehousing, cartels and futures trading; and how the global trade in metals remains shrouded in secrecy.

From this macro picture of the global mining industry, we have zoomed in to the impacts of mining on local populations – the destruction of sacred mountains and traditional livelihoods, and the repression of community democracy and self-determination to serve the profits of faceless foreign shareholders.

The perspectives of indigenous and other people affected by mining should be respected and understood. This doesn’t necessarily mean all mining should cease, but it may have to be dramatically reduced. In Caurem village in Goa for example, where sacred groves have been encroached on by illegal miners, the Gram Sabha has unanimously resolved that if the mines are to be restarted, this should be done through the agency of a multi-purpose cooperative society they have set up.44

The case we are making is for a radical re-assessment of the value of mined resources, taking into account a full life cycle ecological approach which includes ecological and social externalities, and assigns metals their true price. Real pricing of these irreplaceable metals would help to ensure they are used gradually and respectfully, and distributed equally, now and for future generations. In the meantime the opaque nature of the mining industry must be challenged. Governments and communities have a right to know where their resources are going, and at what price, so they can equitably benefit. This powerful information will be the first stage in re-evaluating the role of market forces on the rapidly disappearing precious metals of our planet, and deciding what to do with the remaining deposits before they are all gone.

Further Reading:

Stuart Kirsch, 2014, Mining Capitalism: The Relationship between Corporations and Their Critics University of California Press.

Gladson Dungdung, 2008, Tricks of Trade (‘CSR, as implemented by Arcelor-Mittal in Jharkhand, is more Conspiracy for Snatching Resources than Corporate Social Responsibility’), Tehelka45

Mining Mafia: A threat to democracy.46

Footnotes:

1http://www.sciencedaily.com/releases/2011/09/110907132044.htm

2Samarendra Das, compilation of mined volumes 1821 – 2014.

3www.oecd.org/dataoecd/52/42/46194971.pdf

4World Steel Association. World Steel in Figures, 2013.

5 Windsor, J E, and McVey, J A (2005). ‘Annihilation of both place and sense of place: the experience of the Cheslatta T’En Canadian First Nation within the context of large-scale environmental projects’ Geographical Journal. Volume 171 Issue 2, Pages 146 – 165

6http://www.nytimes.com/2013/07/21/business/a-shuffle-of-aluminum-but-to-banks-pure-gold.html?pagewanted=all&_r=0

7http://www.nytimes.com/2013/07/21/business/a-shuffle-of-aluminum-but-to-banks-pure-gold.html?pagewanted=all&_r=0

9http://www.livemint.com/Companies/9rnumlGUskTqzmzMF15kEK/ArcelorMittal-Tata-Steel-to-start-hedging-iron-ore.html

11http://www.ft.com/cms/s/0/286b295c-820b-11e4-a9bb-00144feabdc0.html#axzz3Lt8zV78q

15http://timesofindia.indiatimes.com/india/Congmen-allege-Rs-4-lakh-crore-mining-scam-in-Odisha-seek-Patnaiks-resignation/articleshow/17107986.cms?referral=PM

16Taxes of mines and minerals – Karnataka State at NIC, 18 Aug 1999. www.kar.nic.in/finance/trc/ch08.pdf

17The Economist, Dec 7th 2013. ‘BlackRock: The monolith and the markets’

http://www.economist.com/news/briefing/21591164-getting-15-trillion-assets-single-risk-management-system-hugeachievement

18http://www.theage.com.au/business/mining-and-resources/iron-ore-wont-reach-us100-per-tonne-again-says-bhp-billiton-20141212-125q3u.html

19http://archive.financialexpress.com/news/national-steel-policy-2005-what-a-damp-squib-/157596/0

21http://archive.financialexpress.com/news/national-steel-policy-2005-what-a-damp-squib-/157596/0

22http://www.dnaindia.com/money/1864791/report-how-jindal-group-landed-mega-iron-ore-deal-in-afghanistan

23http://www.globalwitness.org/library/mittal-steel%E2%80%99s-us900-million-deal-liberia-inequitable-says-new-global-witness-report

24http://www.theguardian.com/environment/2011/jul/04/lakshmi-mittal-arctic-iron-ore

25Michael Ritthoff et al, 2002, Wuppertal 27e, ‘MIPS Resource productivity of products and services’. Wuppertal Institute for Climate, Environment and Energy at the Science Centre North Rhine-Westphalia

26http://zzkptiof.nw.pl/Black%20Rose%20discovery%20triggers%20investigation.htm

27http://gulail.com/vedanta-a-major-player-in-goas-illegal-mining-syndicate/

28According to the Wuppertal Institute.

29Do Agreements Negotiated Under the FREE, PRIOR AND INFORMED CONSULTATION Standards Required by theWORLD BANK and the EQUATOR PRINCIPLES give mining companies an appropriate social LICENCE TO OPERATE? Robert Houston, Rio Tinto Intern, Dundee.

30Mining the truth: The rhetoric and reality of the commodities boom Institute Paper No. 7, September 2011, David Richardson and Richard Denniss

31http://archive.tehelka.com/story_main40.asp?filename=Ws090808tricks_trade.asp

32http://knowledge.wharton.upenn.edu/india/articlepdf/4636.pdf?CFID=182641260&CFTOKEN=18615258&jsessionid=a83078e8bc4af9f839766b3805371b736861 Corporate Social Responsibility in India: No Clear Definition, but Plenty of Debate, Wharton School of the University of Pennsylvania,Aug11

33http://www.kazakhmys.com/en/about_us/board_of_directors

34http://www.independent.co.uk/news/business/analysis-and-features/mining-the-darker-side-of-the-london-market-8213987.html

35http://www.actionaid.org/who-we-are/international-board-members

36 Vedanta’s website (accessed 25/7/11) http://www.southasiasolidarity.org/2011/08/13/strange-bedfellows-for-action-aid/#sthash.Q6GjzZJG.dpuf

40http://www.newyorker.com/magazine/2013/07/08/buried-secrets

42http://archive.tehelka.com/story_main40.asp?filename=Ws090808tricks_trade.asp

43http://orissamatters.com/2013/01/03/orissa-government-should-explain-how-stemcor-completed-95-of-its-project-sans-entitlement/

45http://archive.tehelka.com/story_main40.asp?filename=Ws090808tricks_trade.asp

46http://www.telugudesam.org/tdpcms/scams/mining_threat_book/mining_threat.html